This past Friday, June 3rd, 2016, The Bureau of Labor Statistics released their most recent report regarding new employment data and nonfarm payroll employment which indicates that during May of 2016, it was the smallest increase seen in 28 months.

During May of 2016, there were 144,592,000 payroll jobs within the US, which was up by 1.6 percent, or equivalent to 2.3 million jobs, from May of 2015 (These are all not-seasonally-adjusted numbers).

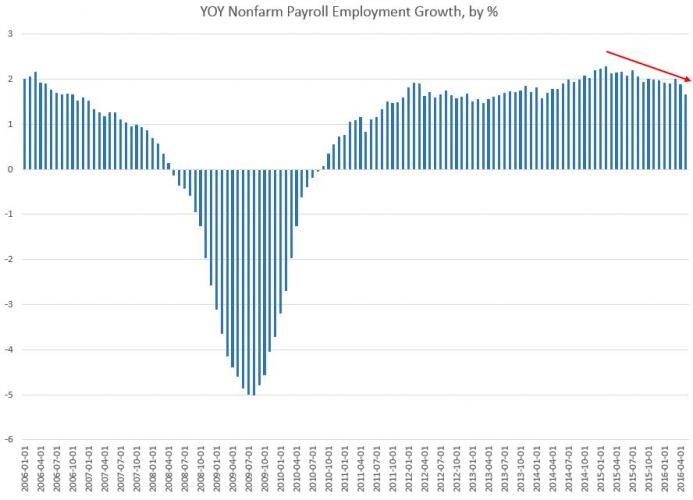

That represents the smallest year-over-year increase that has been reported since February of 2014, at which time payroll jobs increased by 1.57 percent. The largest year-over-year increase, in recent years, was reported during July of 2015, when it was up by 2.18 percent:

Since July of 2015, the general trend in growth has been down. This 1.6 percent remains well below where growth was during most of the 1990’s.

I am not fond of using the seasonally adjusted numbers, since they add an additional layer of ‘needless manipulation’. I do prefer to compare job growth, from the same time of year, over several years.

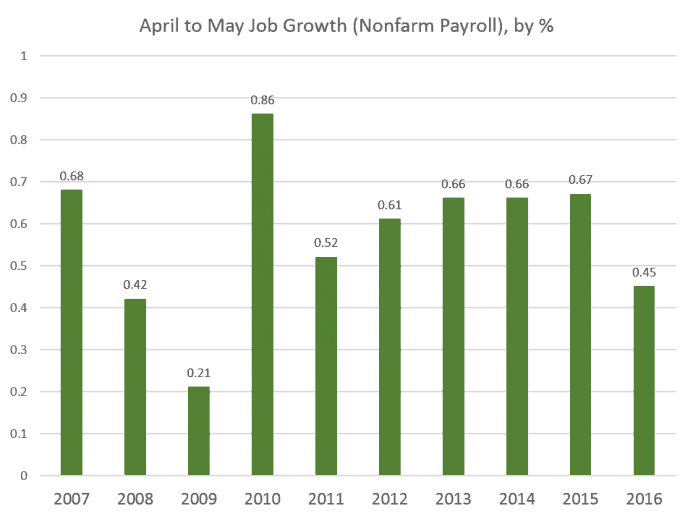

When I do this, I find that the job growth from April to May of 2016, was the lowest April-May growth total since 2009:

From April to May of 2016, there were 651,000 new jobs added, which is a significant drop from that same period of time, last year when 947,000 jobs had been added. Over the past decade, this current year of 2016, in this measure, beats out only 2008 and 2009, both of which were years of ‘economic decline’. Therefore, May of 2016 was the weakest May on record, for job growth, in eight years.

The Secretary of Labor, Tom Perez attempted to blame everything on the Verizon strike. That is a nice “spin”, however, the strike does not explain the obvious ‘decline’ in the year-over-year numbers! The strike might explain why the May numbers dropped off as much as they did, however, it cannot explain the ‘trend’. It is a bit of a stretch to blame this drop from April-May of 2015 to April-May of 2016 on the Verizon strike.

Mr. Perez, however, attempted some other, even less convincing, claims as well, stating that the U.S.’s insufficient mandates on paid family leave means that fewer women are entering the work force, and therefore pushing down the jobs totals. Is this IMPORTANT? The answer is NO! These bad numbers merely reflect our current poor economic situation, today!

In any case, the overall trend should not be a big surprise, as it has always has been weak. It has been dependent on the FED and their low interest rates. In recent quarters, the FED has finally been backed into a corner and has become hawkish. Realizing that more rate cuts are unlikely to occur any time soon, the economy is not receiving the usual FED-manufactured stimulus which investors and companies have both become accustomed to. With the FED talking about the need to raise ‘rates’, who can be surprised that the “recovery” is nonexistent?

The financial news, of the past few weeks, had its cadre of regional FED Presidents attempting to sway markets into believing that the Central Bank was sure to ‘hike’ interest rates during this current month of June 2016.

The jobs report sent ‘shock waves’ throughout the entire financial system. The report printed a jobs number of just 38,000 new employees, which is the lowest single month since the height of the “Great Recession”.

What is even more ludicrous than this, is the fact that the unemployment rate fell to 4.7 percent seeing as 664,000 workers are no longer being counted and included, by the government, within the labor force.

The FED relies heavily on these ‘manipulated’ government jobs numbers, the idea of “data dependency” being used to determine when to ‘hike’ or ‘drop’ interest rates shows the incompetency of a body that supposedly employs hundreds of economists who are dedicated to discover the true state of the economy and of its’ economic data. This in turn, should provide Americans with the reality that not only does the Central Bank have any idea what they are doing, but, more often than not their policy decisions are based on ‘incorrect’ and ‘outdated’ models which have only served to make matters worse, since the “Credit Crisis of 2008”.

The majority of jobs created were either part-time or low-wage service sector oriented. You can bank on the fact that the FED is now more likely to lower ‘rates’ than they are to raise them, going forward!

Today, it is both unlikely and irrational for the FED to raise interest rates either now or in the near future, despite the Central Banks’ recent “moral suasion” on mass media, of a potential rate ‘hike’ occurring as early as this month or possibly next month. The FED continues to create policies in an attempt to protect the economy and stock markets through November of 2016 so as to “spin” the election in favor of Hillary Clinton. This is due to the uncertainty from the presumptive Republican candidate, Donald Trump, who may force the Central Bank into ending its’ mission to fuel ‘stock and housing bubbles’. I, myself, as well as many economists, are seeing the ‘Summer of 2016’ as a dangerous period of time where and when a financial, economic, or monetary ‘collapse’ could take place from any number of ‘flashpoints’. The actions that are now taking place, in the equity markets, are an indication that these ‘fears’ may very well be arriving much sooner than most analysts expect.

The economy is still performing ‘significantly’ below its’ potential:

The problem is that the FED, including other Central Banks, have waited too long and gone too far in their ‘zero interest rate’ policies and ‘quantitative easing’ programs. With all of this nonsensical talk coming from the FED, the debt default levels, especially for credit default swaps on the 10-year Treasury are NOW at their highest level since the FED raised rates by a quarter of a point, back in December of 2015.

The probability of a U.S. default of its’ debt has hit its’ highest point since the FED has hiked rates in December of 2015. This is indicated by the recent dynamics in credit-default swap (CDS) agreements. The expectations that the Central Bank may raise borrowing costs still further, in the coming months, will set off this ‘time bomb’. Since the FED has turned increasingly hawkish of their policy outlook since late April 2016, market volatility has increased, with stocks swinging between gains and losses and U.S. Treasuries sliding along slide with the dollar. “Systemic risks” stemming from the CDS transactions are rising amidst the unfavorable global financial environment. This is not only true in the U.S., but its’ counterparts are also subject to greater turmoil in the coming months, as possible FED hikes, “Brexit” concerns, U.S. elections and faltering global growth are all interconnected factors thereby contributing to the recent spikes in U.S. CDS spreads.

If things follow the FED script, I imagine that next months’ payrolls will exceed ‘tapered down’ expectations and consequently, there will be an upward revision of Mays’ numbers. Will this continue sending the market into exuberance? NO! However, the FED officials will then restart the rate ‘hike’ talks with just enough offsetting uncertainties to mislead everyone while trying to keep the market ‘bubble’ from ‘bursting’.

The financial system is like a giant game of poker with all the major player holding a seven and two off suite (worst hand you can have), yet they are all-in with their chips (money & policies) trying to bluff their way out of this mess.

Things are going to be very crazy over the next 6-12 months and beyond, but until the US large cap stocks breakdown and start a bear market expect tough trading and investing.

Find out what I think the market is doing and where its headed with my ETF Trade Alerts: www.TheGoldAndOilGuy.com

Chris Vermeulen