by Wolf Richter

Consumer confidence plunges the most since 1994.

Britons’ economic sentiment, already sagging since the summer of 2014, has dropped after the Brexit vote at the steepest rate since 1994!

We can’t blame them. The pound sterling plunged 25% over the last 12 months in anticipation of the Brexit vote, and in its aftermath. A bevy of usual suspects, including Goldman Sachs, Deutsche Bank, and Citigroup, are nowproclaiming that the pound could fall another 7% to 11%. Deutsche Bank figures the pound, now at $1.29, could drop to $1.15 by the end of the year.

The initial plunge after Brexit was a reaction to Brexit, they say. But now there’s a second wave of selling on the way in reaction to the Bank of England’s reaction to Brexit.

Forecasters have a history of being wrong, but the current level is real. The destruction of the pound may be good for UK exporters, but it’s terrible for consumers. They buy a lot of imported stuff, and that stuff is about to get more expensive. And forget about going abroad this summer. Can’t afford it anymore.

The financial prognosticators – normally not a doom-and-gloom crowd – weren’t shy about dooming and glooming. Daiwa Capital Markets in a notetitled, “Political Anarchy, Economic Calamity,” added some bitter flavors:

The UK is “in the midst of its deepest political crisis since at least the Second World War, with a vacuum at the top of Government.” At the same time, “the Leave campaigners have no plan how to actually put the Brexit vote into practice.” They’re “displaying a woeful ignorance of the EU’s rules, and appear completely naïve about the motivations and red lines of the UK’s EU counterparts…. And while they think that the EU will be able to cut the UK a special deal, they are deluded.”

All the while, EU Leaders have displayed what is, for them, remarkable unity….

But for the UK economy, “this uncertainty is clearly a massive negative,” with a recession now being “the consensus call”:

We expect a sharp contraction in investment due to the hit on business confidence and significantly lower consumption growth as real incomes get squeezed by rising inflation resulting from the sharp depreciation in sterling (which we expect to fall further from here) and rising unemployment as firms adjust workforces downwards. At the same time, uncertainty will hit construction activity and real estate transactions – and any falls in house prices will serve to put further downward pressure on consumption growth.

And that boost to exports due to the crushed pound? Forget it. It’s “unlikely to boost exports significantly, not least given the uncertainty over the UK’s future trading arrangements.”

The situation could still get worse than Daiwa’s forecast, the note said, with the economy deteriorating more sharply, inflation rising faster, and investment grinding down:

This is particularly true for investment from overseas, where uncertainty about whether the UK will continue to maintain access to the Single Market, a key reason why the UK has the second largest stock of foreign direct investment in the world, is likely to see foreign firms freeze investment plans.

Given the UK’s current account deficit of 6.9% of GDP, this lack of foreign investment “is also potentially dangerous for sterling given the UK’s need for large inflows of foreign capital to pay its way.” At the same time, “attracting the required foreign capital is going to be much more difficult post-referendum.”

Amid this political and economic uncertainty that may hang around “probably years to come,” British consumers have lost their mojo.

According to the special post-Brexit GfK Consumer Confidence Barometer(CCB), the core index plunged to -9, from an already low -1 just before the vote. It was the steepest plunge since December 1994. It was down 16 points from the halcyon days of June 2015, when the index still stood at +7.

These aspects got hammered in particular:

- “General economic situation” over the last 12 months dropped to -19, from -13 just before Brexit, and from +4 a year ago.

- “General economic situation” over the next 12 months, oh my! 60% expect it to worsen; only 20% expect it to improve! So the index plunged 15 points to -29, last seen during the euro debt crisis in 2011 and 2012. It’s down 33 points from a year ago. The index has been deteriorating since the post-Financial Crisis high in the summer of 2014. Another drop of this sort will plant it in Financial-Crisis gloom.

- “Major purchases” dropped 12 points to -3 and is down 19 points from a year ago. “Now is a good time to save” hit the highest point since October 2008. This doesn’t bode well for consumer spending.

The confidence of households with incomes between £25,000 and £50,000 ($32,000-$65,000) took the biggest hit, plunging 16 points. So there will be real consequences, among them:

Our analysis suggests that in the immediate aftermath of the referendum, sectors like travel, fashion and lifestyle, home, living, DIY, and grocery are particularly vulnerable to consumers cutting back their discretionary spending.

With business investment entering the deep-freeze until some modicum of certainty returns to the political and economic environment in the UK and its trading relationships, and with hiring grinding to a halt until further notice, solid consumer spending would be a godsend. But no. With this bashed consumer confidence, gloomy outlook, and intentions to save more and spend less, given all the uncertainty, the UK economy looks to enter a world of hurt – just when global demand is already languishing.

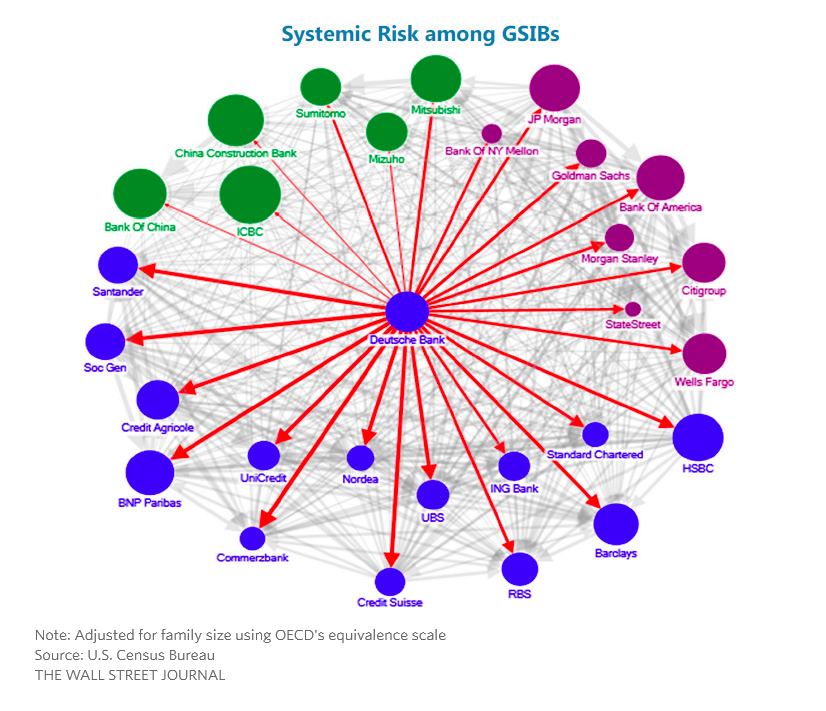

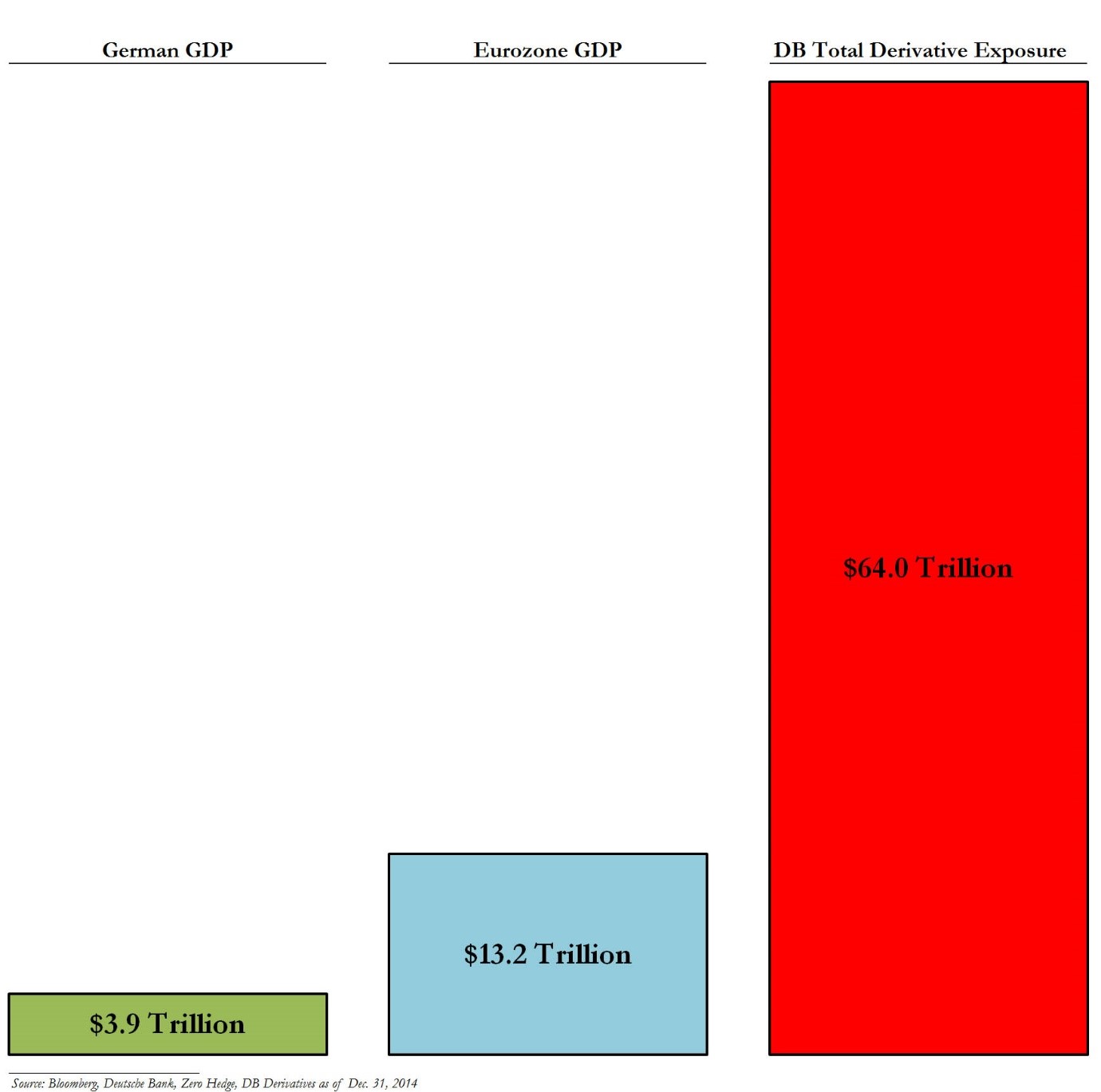

It’s not like Europe doesn’t already have enough problems, including a blooming banking crisis. Among the worst is Deutsche Bank, whose bond-buyback miracle-nonsense earlier this year flopped miserably, and whose shares and CoCo bonds plunged. Read… I’m in Awe at How Fast Deutsche Bank is Coming Unglued

full article: http://wolfstreet.com/2016/07/08/british-consumer-confidence-plunges-post-brexit-economy-to-spiral-down/

Disclaimer © 2010 Junior Gold Report

Junior Gold Report’ Newsletter: Junior Gold Report’s Newsletter is published as a copyright publication of Junior Gold Report (JGR). No Guarantee as to Content: Although JGR attempts to research thoroughly and present information based on sources we believe to be reliable, there are no guarantees as to the accuracy or completeness of the information contained herein. Any statements expressed are subject to change without notice. JGR, its associates, authors, and affiliates are not responsible for errors or omissions.

Forward Looking Statements

Except for statements of historical fact, certain information contained herein constitutes forward-looking statements. Forward looking statements are usually identified by our use of certain terminology, including “will”, “believes”, “may”, “expects”, “should”, “seeks”, “anticipates”, “has potential to”, or “intends’ or by discussions of strategy, forward looking numbers or intentions. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause our actual results or achievements to be materially different from any future results or achievements expressed or implied by such forward-looking statements. Forward-looking statements are statements that are not historical facts, and include but are not limited to, estimates and their underlying assumptions; statements regarding plans, objectives and expectations with respect to the effectiveness of the Company’s business model; future operations, products and services; the impact of regulatory initiatives on the Company’s operations; the size of and opportunities related to the market for the Company’s products; general industry and macroeconomic growth rates; expectations related to possible joint and/or strategic ventures and statements regarding future performance. Junior Gold Report does not take responsibility for accuracy of forward looking statements and advises the reader to perform own due diligence on forward looking numbers or statements.